Eastern

Phone: 0484 300 1100 Ext: 300 1234

Email: socialise@eastern.in

Address: Eastern Condiments No. 34/137 A , NH Bypass, Edapally (P.O), Kochi, India 682024

Open in Google MapsEastern

Be Updated

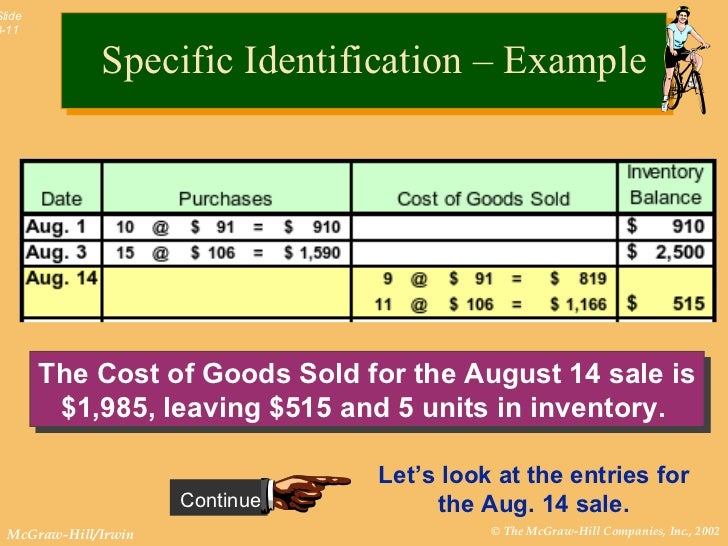

Specific Identification Inventory Method

The specific identification method is an inventory costing technique that assigns the actual cost of each specific item in inventory to the cost of goods sold when the item is sold. The specific identification method is a way of tracking inventory costs without the need for cost flow assumptions. It’s an inventory costing method that suits businesses with high-value, low-volume goods. However, maintaining records can be tedious if your business doesn’t have an organized accounting and information system. Establishing one requires having an accounting software program and a synchronized system of manual records.

Income Tax Calculator: Estimate Your Taxes

A company that might use the specific identification method would be a business that sells fine watches or an art gallery. These requirements can be followed with a simple accounting system, such a spreadsheet. The specific identification accounting method is best used for small business with low unit volumes. It is equally important to understand the disadvantages of specific identification method stock sales. Ending inventory cost – This is the final step where the remaining items are valued at their specific costs. The total purchases of ABC Dealership for the SUVs is $138,515 ($44,235 + $45,030 + $47,300 + $1,200 + $750).

- The company also paid for $1,200 shipping costs and $750 insurance.

- This system is extremely accurate because each piece of inventory can be tracked separately.

- The store uses specific identification to value its inventory by recording the exact price paid for each camera.

- This approach brings with it an array of benefits and challenges, each significant in their own right.

What is the specific identification method for inventory valuation?

When the inventory arrives, each piece is matched the invoice to allocate the cost. The specific identification of inventory methods, or SI Method, is where we specifically identify which items of inventory has been sold. This means that we can expense the exact cost of the item being sold. Through this post, we’ll guide you step-by-step through understanding how this method works to ensure your inventory valuation is spot-on. We’ll unravel the complexities of tracking individual costs and show how this could benefit your bottom line.

Computing Unit Cost per SUV

The ______ ______ Method may lead to profit manipulation as it allows businesses to choose which items to sell to influence ______ ______. After a short break, we reopen the store for a few days and take a final inventory count on the 31st of December just after we lock the doors. Dasan, the black friday of poker stocking clerk, turns that count into the accounting office so they can compare the physical count to the perpetual inventory records. On the 15th of December, preparing for the holiday rush, we bought eight more bats, but the cost has gone up (probably due to higher demand) to $15 each.

Each car has a different dealer cost and a different sales price based on the model and its features. Each of the cars is tracked individually from the time they enter the lot until they are sold. Tracking the cost of each item is crucial for businesses managing expensive equipment. They might label each machine with a serial number and record its purchase price, maintenance costs, and depreciation over time.

Useful for distinguishable and high-value items

This guide discusses how the specific identification inventory method works, who it’s optimal for, its highlights and drawbacks, and how to calculate ending inventory and COGS using it. Because I know the specific units being sold, I can use the specific identification method. Notice this system is exactly the same as if the company was using the periodic system because, under specific identification, we are assigning costs to individual units as they are sold. It can be more complex because it requires detailed tracking of individual items in inventory. Companies often use this method for expensive or unique items where tracking individual costs makes sense.

For an efficient and effective specific identification inventory system, your business must have a detailed inventory stock-keeping system that tracks each item of inventory separately. For instance, individual inventory items might be tracked by unique serial numbers, addresses (for real estate), or title numbers. The specific identification inventory method tracks the costs of individual items of inventory until they are sold to customers. The cost of goods sold (COGS) and cost of ending inventory are determined by the actual cost assigned to each physical unit of inventory. The Specific Identification Method in inventory accounting is crucial for businesses with unique, high-value items like jewelry or custom machinery.

Shaun Conrad is a Certified Public Accountant and CPA exam expert with a passion for teaching. After almost a decade of experience in public accounting, he created MyAccountingCourse.com to help people learn accounting & finance, pass the CPA exam, and start their career. You’ve seen the journal entry, so we don’t need to keep repeating that.

Individual tracking of cost – Each item manufactured or purchased needs to have a proper record of its cost, which will be unique for all in case of specific identification method for inventory costing. The specific identification inventory method is one of the available methods used in inventory management. Clearly the method used to determine which units are sold and which remain in closing inventory determines the value of the cost of goods sold and the closing inventory. As profit depends on the cost of goods sold, the method chosen will affect the profits of a business. The FIFO method uses the earliest unit costs to determine the cost of units sold during the year, or COGS.

With this method, every piece of jewelry, artwork, or any unique product is recorded at its purchase price. This precise tracking helps businesses figure out the correct cost of goods sold and balance their books accurately. For businesses dealing with items like jewelry or art, this method gives a clear picture of financial health.